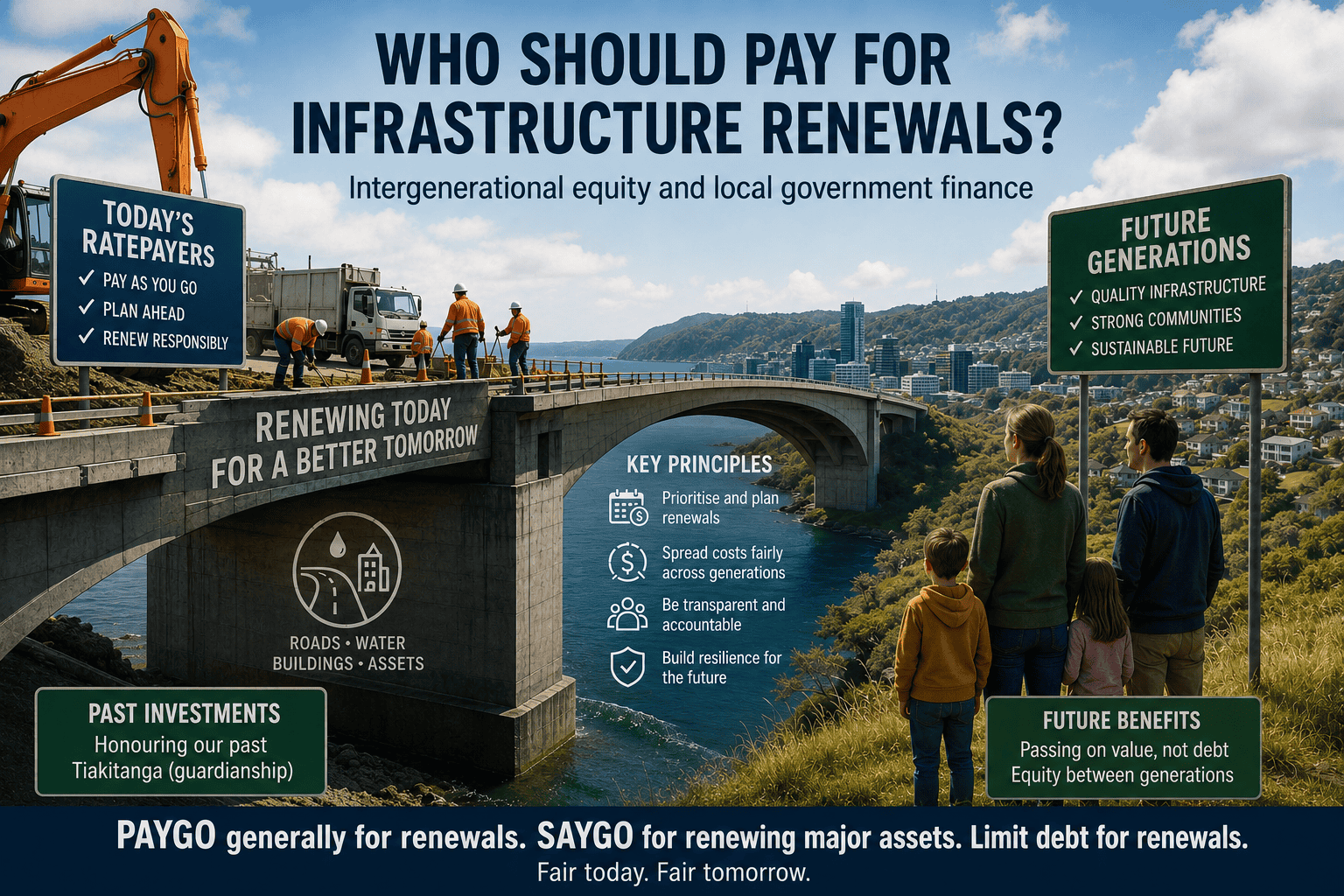

New Zealand local governments face a simple but under-examined question: how should renewal costs be allocated across generations to replace worn out infrastructure? Should today's ratepayers fund renewals as assets wear out (pay as you go, PAYGO)? Should previous generations have saved in advance (save as you go, SAYGO)? Or should future generations pay through borrowing now?

The answer affects rates, debt levels, infrastructure quality, and intergenerational fairness.

We argue that renewals should generally be PAYGO funded, with some room for SAYGO, especially for unusually large assets to avoid future debt-financed renewals. Improvements are needed to accounting and planning practices to support this.

A prompt for this article is a post from Wellington City Council Deputy Mayor Ben McNulty explaining they decided not to fund depreciation for the new expensive convention centre Tākina, saying it’s a call for a future council.

Te Waihanga’s National Infrastructure Plan expects spending on infrastructure to go from just over $20 billion per year to more than $40 billion per year by the 2050s. They argue around 60% of this should go towards renewing and replacing what we already have.

Accounting depreciation was introduced in the 1980s to:

- spread the upfront capital expense for durable assets over their life (not simply the cash paid when the asset was bought) and match it to the benefits the assets provide to better reflect the assets’ performance.

- provide a normative benchmark to help identify abusive deferral of replacements.

- help to stop entities’ profits and surpluses looking needlessly volatile when their capital spending is not steady each year.

However, accounting depreciation remains only a proxy for actual asset consumption and provides limited value in managing long-lived infrastructure networks. For entities supplying long-lived public infrastructure networks, specific asset renewal modelling and standardised reporting is probably more suitable.

The substantive policy question is how should renewal costs be allocated across generations? Should the first generation of ratepayers pay for both the first and the second generations of assets through debt and then savings via “depreciation” (ie, twice)?

Some policy principles about funding renewal investments are provided by the Productivity Commission’s 2019 LG funding and financing inquiry, the Auditor-General’s 2024 benchmarking of local government renewals, and Te Waihanga’s National Infrastructure Plan, but these are not definitive on this intergenerational funding question either. Renewal expenditure should be prioritised, smoothed over time, and aligned with beneficiaries. But this does not narrow the answer to the intergenerational funding question when asset portfolios are highly diversified and multigenerational.

Te Waihanga’s report Is Local Government Debt Constrained? is more suggestive, saying it is better to pay for renewal investments as they are incurred rather than by raising debt (page 8).

The issue is ultimately one of intergenerational equity and democratic accountability. Its resolution is both political and analytical.

First, let’s consider the investment categories other than renewal: levels of service improvements, growth, and resilience. These activities tend to raise land values to capitalize benefits, and so debt-financing that also capitalizes costs is a suitable match (particularly if they target the same land). Further, alternatives to debt-financing are politically difficult. There are poor incentives for earlier generations to give to future, and poor incentives by those receiving generations to apply the savings as intended

Renewal investments tend to be widely diffused and expected, so do not raise land values like the other categories, making debt-financing less suitable. Further, debt-financing renewals would crowd out growth and service level investments and transfer the costs of today's asset consumption to future generations. So, the answer seems to be some combination of PAYGO, ie current generations, or advanced savings (SAYGO), ie earlier generations. In an intergenerational equity sense this could be characterized as ‘honouring your past’ or tiakitanga (guardianship).

PAYGO means paying for renewal capital expenditures each year from revenues that year. It smooths expenditure over time if the asset portfolios are highly diversified and each asset is small share of the portfolio. It’s problematic if there are particularly large assets that probably cannot be renewed from the annual renewal budgets, such as the Wellington Tākina Convention Centre. These assets should have an asset-specific SAYGO component that’s enough to prevent debt finance for renewal being needed. It should be ringfenced to help prevent it being plundered in future.

Local governments could complement PAYGO with SAYGO across the whole renewal programme by running positive savings on average to offset the debt in the other categories. This could help offset the burden of other long-term fiscal commitments being passed to future generations, and address financing risks of sudden failures of major assets. But it is difficult to monitor, communicate, and commit to such efforts having that net effect (rather than just enabling more debt elsewhere).

Recommendations

- Central government bodies and international accounting standards bodies should review the accounting for asset renewal for local public infrastructure providers, including:

- describing the state of assets and estimated remaining life, estimated cost to replace, and estimated likelihood of replacement

- account for future intended renewals, and linking those intentions to asset renewal modelling and renewal plans

- which generations (current, future, or past) are paying for capital renewal expenditures.

- Central and local governments should establish a framework requiring entities to prepare, maintain, and publicly explain departures from asset renewal plans.

- Local governments (and their agencies) should commit to limit any use of debt finance for renewal expenditures, except where exceptional circumstances justify it.